In partnership with

The Volatility Cone: A Quant's Tool for Mapping Price Uncertainty

Get what you want from TV advertising

What you want from TV advertising: Full-screen, non-skippable ads on premium platforms.

What you get: "Your ad is on TV. Trust us."

Modern, performance-driven CTV gets your TV ads where you want with transparent placement, precision audience targeting, and measurable performance just like other digital channels.

TV doesn't have to be a black box anymore.

② One strategy in this book returned 2.3× the S&P 500 on a risk-adjusted basis over 5 years.

Fully coded in Python. Yours to run today.

The 2026 Playbook — 30+ backtested strategies,

full code included, ready to deploy.

20% off until Tuesday. Use APRIL2026 at checkout.

$79 → $63.20 · Expires April 7.

→ Grab it before Tuesday

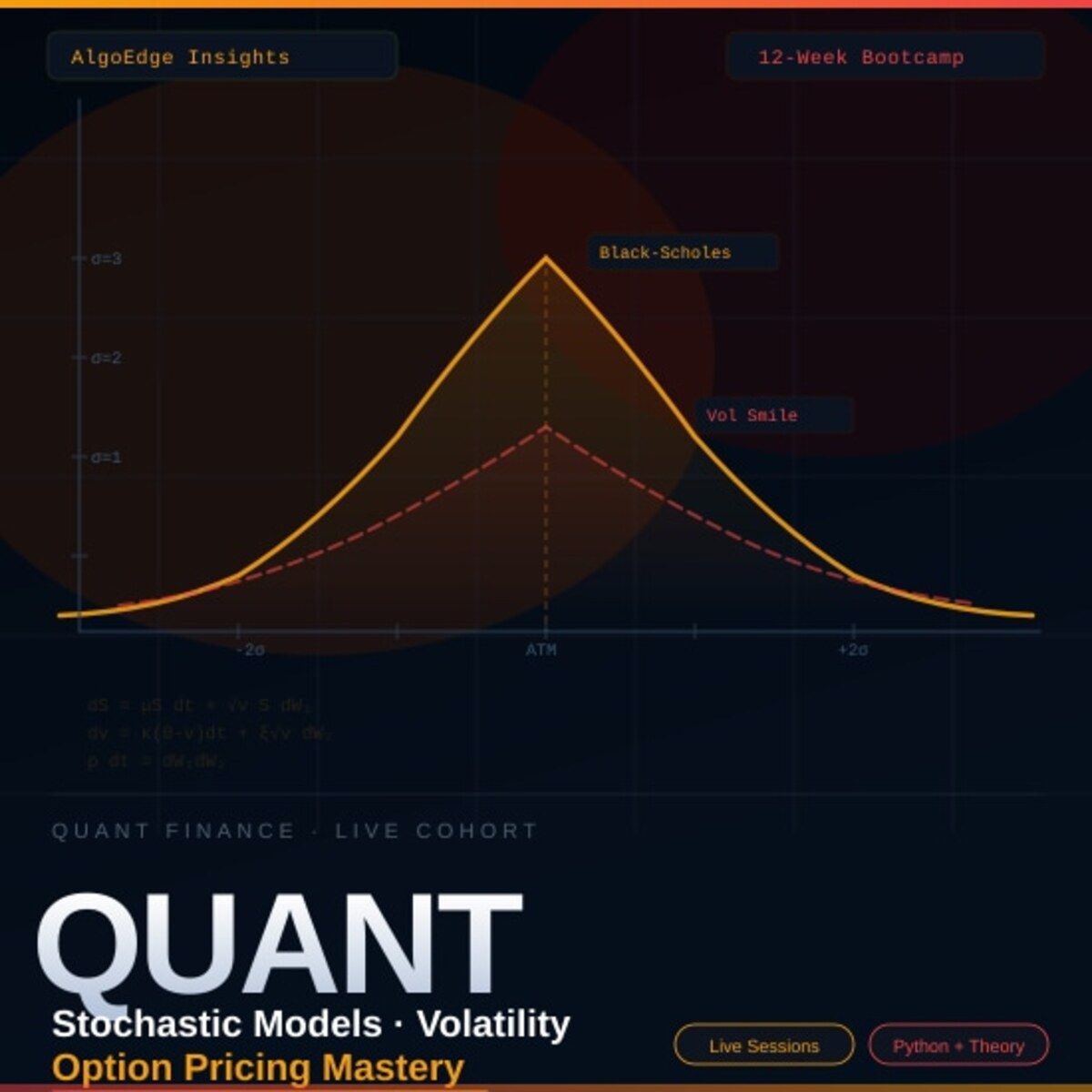

⑤ Most quant courses teach you to watch. This one makes you build.

Live. Weekly. With feedback on your actual code.

The AlgoEdge Quant Finance Bootcamp — 12 weeks of stochastic models, Black-Scholes, Heston, volatility surfaces, and exotic options. Built from scratch in Python.

Not pre-recorded. Not self-paced. Live sessions, weekly homework, direct feedback, and a full code library that's yours to keep.

Cohort size is limited intentionally — so every question gets answered.

→ Before you enroll, reach out for a 15-minute fit check. No pitch, no pressure.

📩 Email first: [email protected]

Premium Members – Your Full Notebook Is Ready

The complete Google Colab notebook from today’s article (with live data, full Hidden Markov Model, interactive charts, statistics, and one-click CSV export) is waiting for you.

Preview of what you’ll get:

Inside the SMA Strategy Lab

📥 Auto-fetches GSPC.INDX data — Integrated with EODHD APIs to pull 10 years of historical daily price action.

📡 Low-Pass Filter Logic — Explains how to separate high-frequency market "noise" from the underlying "signal" using DSP principles.

🛡️ Bias-Free Signal Engine — Implements causal math using

.shift(1)to strictly eliminate lookahead bias and "seeing the future."⚖️ Lag-Length Analysis — Quantifies the trade-off between smoothness and responsiveness ($Lag \approx \frac{N-1}{2}$) across 5 different time horizons.

🔄 Multi-Window Backtester — Runs 10-day, 20-day, 50-day, 100-day, and 200-day Simple Moving Average (SMA) strategies simultaneously.

📊 Risk-Adjusted Scorecard — Calculates Sharpe Ratios, Annualized Volatility, and Max Drawdowns for every window.

📉 Drawdown Heatmaps — Visualizes the peak-to-trough pain for each strategy to identify which window survives market crashes best.

📈 Comparative Visualization — Generates 6+ high-resolution charts, including equity curves, rolling volatility, and performance bar charts.

🗃️ Performance Matrix — Consolidates all results into a clean, rounded

pandastable ready for export or further quantitative research.

Free readers – you already got the full breakdown and visuals in the article. Paid members – you get the actual tool.

Not upgraded yet? Fix that in 10 seconds here👇