In partnership with

The Volatility Cone: A Quant's Tool for Mapping Price Uncertainty

How Jennifer Aniston’s LolaVie brand grew sales 40% with CTV ads

For its first CTV campaign, Jennifer Aniston’s DTC haircare brand LolaVie had a few non-negotiables. The campaign had to be simple. It had to demonstrate measurable impact. And it had to be full-funnel.

LolaVie used Roku Ads Manager to test and optimize creatives — reaching millions of potential customers at all stages of their purchase journeys. Roku Ads Manager helped the brand convey LolaVie’s playful voice while helping drive omnichannel sales across both ecommerce and retail touchpoints.

The campaign included an Action Ad overlay that let viewers shop directly from their TVs by clicking OK on their Roku remote. This guided them to the website to buy LolaVie products.

Discover how Roku Ads Manager helped LolaVie drive big sales and customer growth with self-serve TV ads.

The DTC beauty category is crowded. To break through, Jennifer Aniston’s brand LolaVie, worked with Roku Ads Manager to easily set up, test, and optimize CTV ad creatives. The campaign helped drive a big lift in sales and customer growth, helping LolaVie break through in the crowded beauty category.

② One strategy in this book returned 2.3× the S&P 500 on a risk-adjusted basis over 5 years.

Fully coded in Python. Yours to run today.

The 2026 Playbook — 30+ backtested strategies,

full code included, ready to deploy.

20% off until Friday. Use SPRING2026 at checkout.

$79 → $63.20 · Expires March 21.

→ Grab it before Friday

⑤ Most quant courses teach you to watch. This one makes you build.

Live. Weekly. With feedback on your actual code.

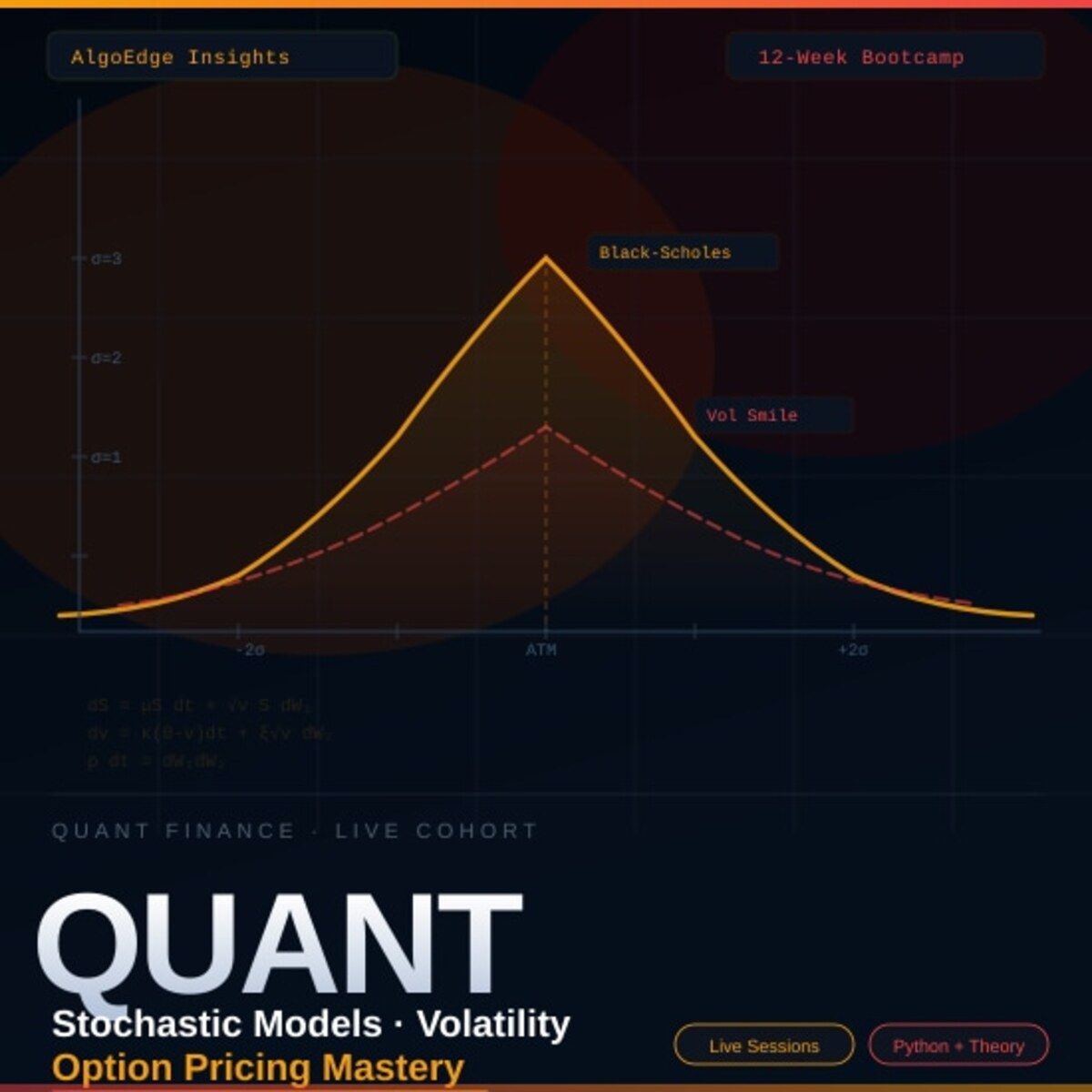

The AlgoEdge Quant Finance Bootcamp — 12 weeks of stochastic models, Black-Scholes, Heston, volatility surfaces, and exotic options. Built from scratch in Python.

Not pre-recorded. Not self-paced. Live sessions, weekly homework, direct feedback, and a full code library that's yours to keep.

Cohort size is limited intentionally — so every question gets answered.

→ Before you enroll, reach out for a 15-minute fit check. No pitch, no pressure.

📩 Email first: [email protected]

Premium Members – Your Full Notebook Is Ready

The complete Google Colab notebook from today’s article (with live data, full Hidden Markov Model, interactive charts, statistics, and one-click CSV export) is waiting for you.

Preview of what you’ll get:

Inside:

📥 Auto-downloads ASML data from Yahoo Finance — change the ticker to any stock you want

📊 Volatility analysis — daily return distribution + rolling 30-day annualized volatility chart

⚙️ Monte Carlo engine — 10,000 simulated price paths using Geometric Brownian Motion

🔀 Two models side by side — Historical Volatility vs BSM Implied Volatility

📈 Confidence cone chart — 68% and 95% intervals with median and mean paths

🎯 Probability calculator — P(above threshold), P(below threshold), P(in range)

📉 Final price distribution — histogram of all 10,000 simulated outcomes with colour-coded zones

💾 Saves 3 charts as PNG files ready to download

Free readers – you already got the full breakdown and visuals in the article. Paid members – you get the actual tool.

Not upgraded yet? Fix that in 10 seconds here👇